Skip to content

Skip to content

Wells Fargo: Will There Be A Dividend Increase In 2023? (WFC)

")

Michael M. Santiago

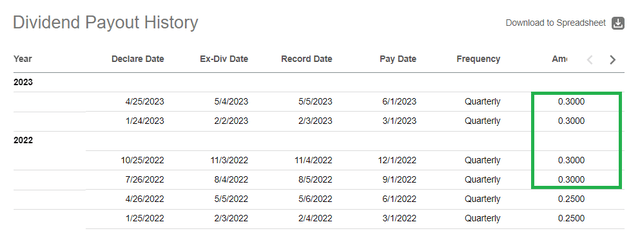

Wells Fargo & Company (NYSE:WFC) recently went ex-dividend for its quarterly dividend of 30 cents per share, marking it the 4th consecutive time the company has paid the same dividend. Naturally, for dividend growth investors like myself, that brings up the questions, “Will there be a dividend increase?” and “If so, by how much?”.

WFC Dividend (Seekingalpha.com)

I will acknowledge right away that Wells Fargo and most banks in general have a spotty record when it comes to their dividend history. Irrespective of the underlying cause, be it the financial crisis of 2009 or the COVID triggered stress in 2020, Wells Fargo’s dividend has ebbed and flowed, primarily dictated by macro environment. The quarterly dividend was 34 cents before the reduction to 5 cents in 2009. From there, the dividend had worked its way to 51 cents in 2019 before being reduced to 10 cents in 2020. Right now, the dividend is back to 30 cents, which brings it back to 2013 level. In short, is it wise to look forward to a dividend increase when a new banking crisis is on the horizon?

I am presenting a few reasons why I believe Wells Fargo will indeed announce a dividend increase over the next few months. Let us get into the details.

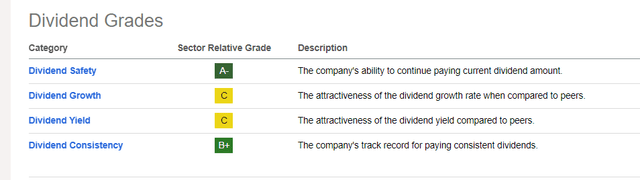

- They can afford it: Wells Fargo is expected to earn $4.76/share for FY 2023. That places the current payout ratio at a comfortably 25% based on annual dividend of $1.20/share. Earnings are expected to grow at a meager 5%/yr over the next 5 years but even that should give the company enough room to hand out small dividend increases. Seeking Alpha’s quant ratings gives Wells Fargo fairly handy grades ranging from C to A- in the 4 categories tracked for Safety, Growth, Yield, and Consistency.

WFC Dividend Grade (Seekingalpha.com)

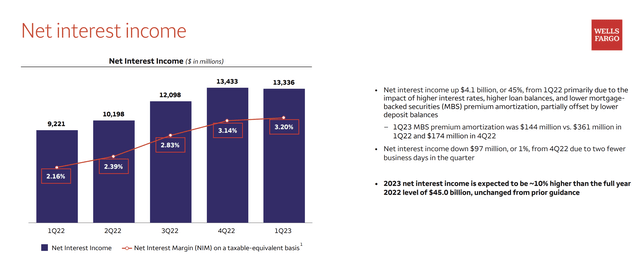

- Going in the right direction: The company’s recent earnings report was encouraging, with Net Interest Income (“NII”) blazing up 45% YoY to $13.3 billion, thanks to the high interest environment. For the full year, Wells Fargo has guided to $45 billion in NII. Noninterest expense was down $175 million in Q1, indicating a tighter reign over expenses.

Wells Fargo Net Interest Income (wellsfargomedia.com)

- Goliaths are winning over the Davids: The recent financial crisis is centered around regional banks (Davids) and it is the large banks like Wells Fargo (Goliaths) that are coming to their rescue. As we saw recently with JPMorgan Chase & Co. (JPM), the large banks are eating up the regional players at a discount that would have been unimaginable a few short months ago. Overall, when the dust settles, the large banks are likely to come out stronger than they were at the beginning of the regional bank crisis.

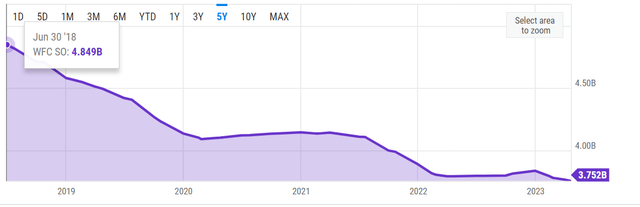

- Shareholder Friendly: As shocking as that may sound to some because of their dividend slashing history, Wells Fargo is a shareholder friendly company. A testament to that is the fact that despite the dividend getting slashed in 2020, the company’s shares outstanding has been on a steady decline as shown below. In the last five years, total shares outstanding has gone down by almost 22.50%. Buybacks not only increase a company’s Earnings Per Share but also saves money as no dividend is owed on the repurchased shares. In the recent quarter, Wells Fargo repurchased $4 billion worth of shares amounting to 86.4 million shares, which saves them $26 million each quarter based on current quarterly dividend of 30 cents.

Wells Fargo Shares (YCharts.com)

- Peer Pressure: Bank of America (BAC) has now paid the same quarterly dividend for four consecutive quarters and their numbers look good enough for a dividend increase this year, after an increase in 2022. Morgan Stanley (MS) has also paid the same quarterly dividend 4 consecutive times and based on last year’s announcement, is likely to announce an increase in a month or two. JPMorgan and Citigroup Inc. (C) have paid the same dividend for almost two years now. Wells Fargo (or any other bank for that matter) would love to be a winner in the upcoming stress test, just like Wells Fargo was in 2022. If Wells Fargo’s scores come out acceptable, expect the company to announce a dividend increase.

Conclusion

While I am unlikely to ever see bank stocks as long-term dividend growth holdings, they can and have been part of my portfolio as cyclical trades that also happen to pay (increasing) dividends when the macro environment is not utterly in shambles. I don’t believe the economy is in shambles yet while also believing that the large national banks are battle and scrutiny hardened at this point. I fully expect Wells Fargo to announce a dividend increase. I am glad that this report agrees with me and has identified Wells Fargo as the bank that will award the 2nd highest dividend increase to shareholders in 2023. I’d like and recommend Wells Fargo to be cautious though by announcing a small dividend increase (say 32 cents/quarter) and retain enough dough to pick up regional banks on the cheap a la JPMorgan Chase.

Lastly, it doesn’t hurt to initiate or add to your position when the stock is trading at less than 8 times forward earnings, especially when you expect a dividend increase on top of a 3.20% yield.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/thenational/NCGI2POJUMH75OPWNUNUZBBGKQ.jpg "How Nigerian immigrants outpaced Indians and South Africans to be most educated in Britain")

Stock: Still Cautious Despite Solid Results")